Nutraceutical products present an opportunity for pharma companies to introduce a new revenue source relatively quickly. The barrier for entry is low, mainly due to 3 reasons:

- less demanding regulatory requirements

- lower cost of development

- shorter time to market

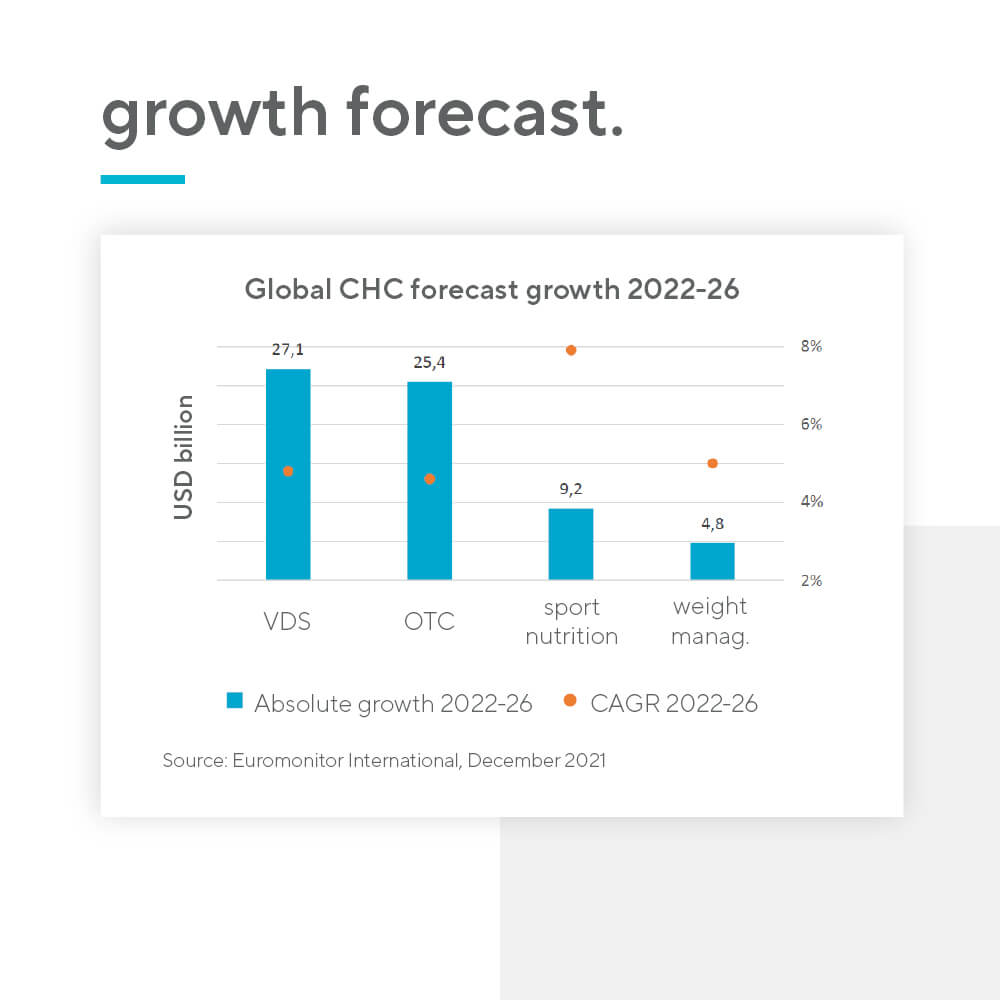

According to IQVIA, the typical time to market for a new indication in OTC drugs is 2-4 years, whereas for nutraceuticals the number is significantly lower – only 1-2 years. Furthermore, vitamins and dietary supplements (VDS) are a high-volume and high-growth category, due to their tapping into the rising preventative health trend. Unsurprisingly, the category is already larger than OTC drugs. There is also no price regulation for nutraceutical products.

")